Co-authored by Anupriya Nair & Sourya Reddy

The concept of Microfinance has seen much success all over the globe. In India, through Self-help Groups (SHGs), it has proven to be an effective tool for empowerment as well. What is basically a small group of people coming together as a small collective to address each other’s financial needs, has facilitated a trustworthy, timely and responsible flow of credit to those most in need of it. While SHGs are created to primarily meet credit needs, the platform it creates can be used, directly and indirectly, to meet other developmental challenges.

One of India’s most consistent problems has been that of improving primary education outcomes. While the blame game has shifted from government to government we are still far from meeting the goal of “education to all”. Can our vast microfinance system help in any way?

Understanding the Link

The connect to education seems fairly intuitive; microfinance loans provide the means for families to enrol and keep their children in school. Several studies have backed this up, showing that the variability of income, rather than the household’s poverty level, is a stronger determinant of whether or not a child is in school. What this means is that the more a household’s income fluctuates is connected to decreased attendance. Microfinance credit brings some comfort to this fluctuation. Infact, in a study of microfinance in Africa, Molsey and Rock found that with any kind of increased income, education was one of the first things parents would spend on.

An increased access to credit allows parents to do basic things, like pay fees for better schools, buy uniforms, school supplies, transportation to school, etc. With more disposable income, parents will also be able to acquire better nutrition; children with a healthier diet will no doubt fare better at school than those who are insufficiently nourished. In addition to access to credit, SHGs have provided great support for members; from an easy transfer of knowledge to emotional support and developing a sense of community.

SHGs and Microfinance in general have seen great success in India; in 1992, the National Bank for Agricultural and Rural Development (NABARD) started linking SHGs with banks, to borrow from the bank as a group. Through what came to be known as the Self-Help Group Linkage Programme, NABARD had launched what blossomed into the world’s largest micro-credit program.

Taking on the Indian Challenge

Over the past few years, the Indian microfinance ecosystem has seen a huge boom. With several hundred institutions providing these services, as of 2017, close to 40 million have benefitted from this system.

India’s education journey, however, is far from this kind of success, for a list of reasons known all too well.

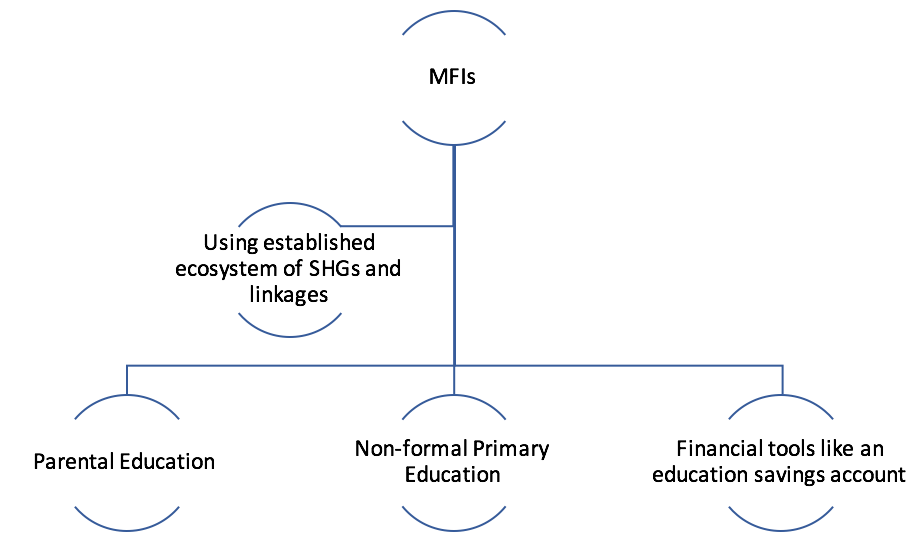

With the huge presence and impact that SHGs and MFIs have, embedding education as a central objective in microfinance programs may accelerate progress in the area.

Bangladesh’s Rural Advancement Committee (BRAC) is a great example of the same. This group-based microcredit program began a series of experimental, non-formal primary schools (came to be known as the Non-Formal Primary Education, or NFPE, Programme,) in 1985. With flexible schedules, localized learning, and special training for locally recruited teachers, over 12 million students have graduated from BRAC-run schools, and close to 1.8 million are currently enrolled. 93% of those who graduate from this program enter the formal education system!

What’s really interesting about their model is the efforts undertaken to educate the parents first. Before the NFPE program was established, BRAC’s Rural Development Programme had a compulsory functional education course for every participant. Aimed at creating politically and socially conscious citizens, it included an optional literacy component. The success of this led to the creation of the NFPE, with the parents as the central demanding force.

Why is educating parents a key aspect? Simply because future generations will reap the benefit; once any generation is educated, they will demand better education for their children, with demand increasing for each passing generation. A study of MFIs in Bolivia found that when MFIs include an educational program for participants of a program (credit-cum-education programs), the perceived value of education for their children increases, heightening demand for child education.

A big driving force behind ensuring the success of parental education, and indeed, the primary education problem, is educating the mother. A UNICEF study of 55 countries found that “children of educated women are much more likely to go to school, and the more schooling the women have received, the more probable it is that their children will also benefit from education.”

Understandably, this is an important factor in the Indian context; in a situation where the girl child’s education is often foregone for the boy’s, where the gender gap in all fields is as big a problem, focusing on basic non-formal education for the mothers can go a long way. This has been seen in BRAC’s case works to remedy Bangladesh’s education gender gap; Mushtaque, Chowdhury and Bhuiya find that “70% of the BRAC school attendees are girls and come from the poorest sections of the community to whom the formal public sector schools are less accessible.”

Getting Creative

By actively targeting education outcomes in communities where they operate, MFIs and SHGs can create and cater to the demand for education. Combining this with tools like an educational savings account — an account designed with tax benefits to cover educational expenses for the children — may prove to be a game-changer.

By making education objectives a key aim, and not an indirect benefit of the microfinance ecosystem, there is a real chance to see some improvement.

The Indian education crisis is real, and for all our talk of a demographic dividend, the improvement in outcomes is far too slow. With such a widespread, resourceful and well-connected micro-credit ecosystem in place, we can do more for our future generations, and take a few, concrete steps towards an education for all.

Featured image courtesy Jaimoen87|CC BY-SA 3.0

#/media/File:A_community_health_worker_conducting_a_survey_in_the_Korail_slum,_Bangladesh_(8630810827).jpg){kind=link}